The Southern Baptist Convention (SBC) is on the verge of a radical transformation. The denomination as we’ve known it, loved it, served it, and funded it may not exist in recognizable form in a generation. The institutions will still be around, but will they hold to our same Baptist doctrine, conservative theology, and urgency to reach the world with the true gospel?

In the 1990s and early 2000s, dozens of state Baptist institutions that had drifted into theological liberalism separated from their state conventions, taking their real estate and endowments with them. Previous generations of faithful Southern Baptists built and supported those institutions with their tithe dollars, and then one day they were just gone. Furman University is one such institution. South Carolina Baptists founded the school and supported it for generations, and our flagship seminary—The Southern Baptist Theological Seminary—was birthed out of its theology department. You’d never know it today. The university is now fully secularized, enthusiastically promoting DEI initiatives and LGBTQ+ ideology. A professor recently led students on a Queer History tour to San Francisco.

The exodus of Baptist institutions did not happen because the churches went liberal, but because they lost control of the institutions. Here’s how it often played out. First, the institutions began taking large amounts of funding from outside their state convention. Then, they argued that since the convention does not fully fund the institution, it should not elect all the trustees. Eventually, trustee boards either outright voted to leave their state convention (e.g. Furman) or reorganized their boards to be self-perpetuating rather than appointed by the convention (e.g. Baylor and Mercer).

Today, our churches have remained doctrinally faithful but have not been denominationally vigilant. Therefore, the national convention faces the danger of the very same fate. In the summer of 2025, SBC messengers approved a new Business and Financial Plan that opens the floodgates to outside funding. If messengers do not reclaim oversight of who’s funding our institutions, we risk our entities abandoning the churches of the Southern Baptist Convention to serve their new patrons, whether those be individual mega-donors, political activist groups, governments,1 or simply non-Baptists. For he who holds the purse always holds the strings.

1. Jon Whitehead, “Follow the Money: Is NAMB Trading Baptist Convictions for Federal Grant Funding? SBC Elite’s Defense of Taking Refugee Money from Biden Admin Strangely Avoid Main Issues,” Center for Baptist Leadership, February 18, 2025.

It is not alarmism to warn that our convention’s gospel ministry is at stake. It’s just paying attention to history and human nature. The lure of money is strong. Once institutions begin fishing in the blue oceans of outside funding, without the convention approval and knowledge that our previous business plan required, our mission becomes in danger of drowning. Or, to change the metaphor, they may start following that money—right off the doctrinal cliff. It’s happened before.

A Proposed Solution . . . Again

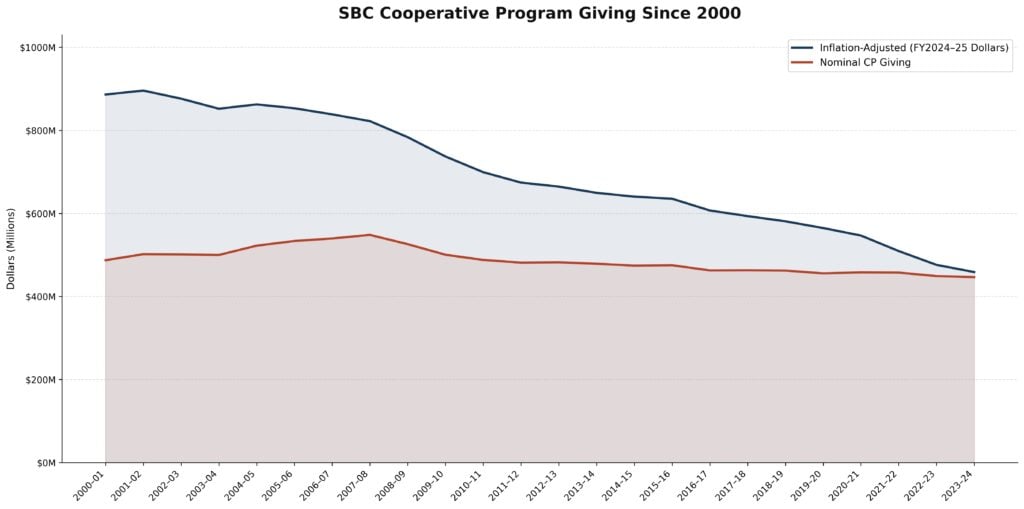

For the last three years, I have worked to secure increased financial transparency and accountability in our convention. I’ve done this because I want to see increased cooperation for the sake of our shared gospel mission. I’ve made the case that Great Commission cooperation among Southern Baptists runs on trust,2 and that the Southern Baptist Convention leadership’s unwillingness to provide sufficient financial transparency is eroding that trust quickly. The numbers bear this out. Designated giving directly to SBC entities continues to increase, general Cooperative Program receipts remain below budget, and, as Figure 1 shows, when adjusted for inflation, our mission boards are receiving almost $130 million less than they were in 2013.3 If you just look at the raw numbers, it may appear that giving is only slightly down. But from an inflation perspective, we have suffered a dramatic decrease in year-to-year total giving (see Figure 1 below and Appendix A). We can only speculate about the factors that have contributed to this massive downturn in financial support, but I believe the crisis of trust is at the heart of the issue. Regardless, this current trajectory is not sustainable to carry out our mission to reach the whole world with the good news of Jesus Christ.

2. Rhett Burns, “Baptist Cooperation Runs on Trust—And Trust Demands Transparency,” Center for Baptist Leadership, March 12, 2024. The Cooperative Program is the SBC’s unified funding mechanism through which member churches contribute a percentage of undesignated receipts to support denominational missions, theological education, and ministry efforts at both state and national levels.

3. See page 12 of the 2025 Book of Reports for a comparison. Southern Baptist Convention Executive Committee, Book of Reports of the 2025 Southern Baptist Convention, Prepared for the One Hundred Sixty-Seventh Session, One Hundred Eightieth Year (Nashville: Southern Baptist Convention Executive Committee, 2025).

Figure 1. SBC Cooperative Program giving in nominal dollars (red) and inflation-adjusted FY2024–25 dollars (blue). Shaded area in blue represents the difference between nominal reported giving and real purchasing-power equivalent when adjusted for inflation.

One solution to restoring trust is simple in principle: give SBC churches and messengers the same basic levels of financial disclosure that other nonprofits offer to the public. Therefore, at the 2023 annual meeting in New Orleans, I moved to amend the Business and Financial Plan to require entities to publish financial information in the same scope and detail as is found on the IRS Form 990, the standard tax return nonprofits are required to file. Due to a religious exemption, SBC entities are not required by law to file a 990, and this motion would not change that exemption at all. Rather than reporting anything to the IRS, this motion would have required our entities to simply give that same basic level of disclosure to churches and messengers for the sake of accountability and trust.

Stonewalled

What followed was two years of frustration, trying to secure a messenger vote on the motion.

First, I was invited to speak to my motion at the September 2023 Executive Committee meeting in Nashville, only for that invitation to be postponed until the following February of 2024. At the time, due to the resignation of the then-interim president, I was told the finance committee would not take up my motion until the next meeting. Fair enough, but I later found out that they did take up discussion of my motion in September 2023, allowing the entity heads to come in and be the first to speak to it, thus poisoning the well against it. I did attend the February 2024 meeting and was given five minutes to speak in favor of the motion plus a few minutes to answer questions before the committee entered into executive session so they could discuss the merits of transparency behind the secrecy of closed doors.

Second, the finance committee did not decide on my motion until the day before the June 2024 annual meeting in Indianapolis, at which point they declined to give messengers an opportunity to vote on the motion. Instead, the committee promised to review the Business and Financial Plan to determine ways to “enhance transparency” and to bring a recommendation to the 2025 annual meeting in Dallas.

Their plan to “enhance transparency” turned out to be a complete rewrite of the Business and Financial Plan that did not enhance transparency at all, but rather codified financial obscurity.4

4. Rhett Burns, “The Emperor Has No Clothes: How The EC’s ‘Enhanced Transparency’ Plan Codifies Increased Obscurity,” Center for Baptist Leadership, March 27, 2025.

A Trojan Horse

The new plan, drafted by entity heads, did two things that should alarm every Southern Baptist who cares about the health of our cooperative mission.

First, it stripped messengers of rights to crucial financial information. For example, under the old plan, members of SBC churches had a right to request salary structures from entities. The new plan gutted even this modest provision.

Second, and more consequentially, it opened the floodgates for entities to raise funds from outside the SBC while simultaneously removing the requirements for approval from and reporting to messengers about such outside fundraising. In other words, under the new plan, SBC entities need no longer be primarily funded by SBC churches.

Thus, while purporting to enhance transparency and streamline the Business and Financial Plan, the actual effect of the new plan is to set the conditions for fundamentally changing our convention.

Dallas

The recommendation to adopt a rewritten Business and Financial Plan did give the opportunity for the messenger body to have a floor debate and vote on transparency for the first time, as the Executive Committee’s recommendation would be subject to debate and amendment.

I had previously tried to warn of the many problems with the new plan, but believed we had a better shot of amending the plan than outright defeating it.5 So, at the 2025 SBC Convention in Dallas, I moved to amend the new plan to include 990-level transparency. But Executive Committee president Jeff Iorg quickly took to the platform microphone to speak against the motion with a speech marked by fearmongering, fallacy, and flat-out falsehood.6

5. Rhett Burns, “Murder on Music Row: The New Business & Financial Plan Might Kill the Cooperative Program,” Center for Baptist Leadership, June 5, 2025.

6. See Southern Baptist Convention, “SBC 25 – Wednesday Morning,” filmed June 11, 2025, at the 2025 SBC Annual Meeting, Dallas, TX, video, timestamp 3:12:27, Baptist Press, June 12, 2025. For example, Iorg attempted to instill fear about federal intervention, invoking a decades-old First Amendment case to suggest that voluntary financial disclosure to convention messengers would invite federal oversight– a non-sequitur, since disclosing financials to denominational stakeholders has no bearing on government jurisdiction. Next, he claimed that 990-level reporting would create legal conflicts between entity trustees and the convention, offering no supporting evidence and ignoring the fact that state Baptist universities with messenger-elected trustees file 990s routinely without such conflicts. Finally, Iorg closed by claiming that SBC transparency practices are “more robust than outside of Southern Baptist life”– a statement that is patently false because SBC entities refuse to meet the baseline disclosure standards required of most nonprofits. For a more detailed analysis of Iorg’s speech, see Center for Baptist Leadership.

After a few speeches for and against, a messenger called the question and messengers quickly voted to pass the new plan with no further debate on its merits or dangers. The amendment failed. And that’s how Southern Baptists voted to fundamentally change their convention without even realizing it.

Two Sides of the Same Coin

How did this new plan fundamentally change our denomination? By removing funding control and financial accountability from messengers, the new Business and Financial Plan creates conditions for real doctrinal drift. Financial accountability and doctrinal accountability are two sides of the same coin. You don’t get the latter without the former. Once Southern Baptist churches are no longer the primary funders of an entity, those churches will lose the ability to maintain long-term doctrinal accountability over that entity. The state Baptist institutions lost in the early 1990s provide cautionary examples of how this has played out in our own history. Recent revelations, as documented in Megan Basham’s Shepherds for Sale, of leftist activist money flowing into SBC entities confirm this is no theoretical concern.7

This reality is why so much more was at stake in June 2025 than most messengers realized. The movement for greater financial transparency was never about a voyeuristic curiosity about executive salaries. It’s always been about proper accountability in service to our shared mission to reach the whole world with the gospel of Jesus Christ. Now, the long-term viability of that mission is in jeopardy because the guardrails of doctrinal accountability to our churches have been bulldozed. Once doctrine is degraded, the mission follows suit.

7. Rhett Burns, “Transparency, Trust, and the Great Commission: It’s Time to Open the Books of the ERLC (and SBC),” Christ Over All, March 18, 2025. See also Megan Basham, Shepherds for Sale: How Evangelical Leaders Traded the Truth for a Leftist Agenda (New York: Broadside Books, 2024).

A Path Forward

So, what can be done?

It’s not too late to course correct. At any point, messengers could vote to revise the Business and Financial Plan to restore accountability to messengers and churches, including amending the plan to provide 990-level disclosure. That would require either deft and courageous leadership from within convention executives or an enormous amount of political will from the messenger body. The problem is that, to a man, not one current SBC entity head or officer of the convention has publicly indicated any interest in restoring accountability through financial transparency. And the messenger body lacks the will to overrule denominational leaders that are on the platform during the annual meeting.

Therefore, I do not see an immediate path to amending the Business and Financial Plan. But that does not mean transparency advocates are without options; it just means we must be patient and prudent. One effective way to chart a course correction for Southern Baptists is to elect officers who support increased financial transparency and accountability.

One of the candidates for president has publicly indicated such support. Pastor Willy Rice lists “Denominational Accountability” as the second of his seven pillars for Baptist renewal,8 even proposing the idea of a Denominational Accountability Task Force to study and recommend actions for increased financial transparency, entity reporting, and the role and responsibilities of trustees.

8. Pastor Willy Rice’s Baptist Renewal initiative identifies seven pillars guiding his vision for renewal within the SBC: Convictional Clarity, Denominational Accountability, Missional Integrity, Cultural Responsibility, Biblical Unity, Global Intentionality, and Spiritual Vitality.

Electing a president who supports increased transparency and accountability, and voting for that president to form a Denominational Accountability Task Force are two achievable objectives for transparency advocates to aim for in Orlando in June 2026. They do not themselves secure the financial transparency needed to restore trust and accountability in the convention. But they can help create the necessary conditions for securing that transparency in the future.

The Real Loss

We are not a financially healthy denomination. Leadership is out of touch, and the messengers are largely out to lunch. Everywhere one looks the warning signs are flashing that the Cooperative Program is dying, but nobody wants to say so publicly. Instead, convention leaders trumpet the Cooperative Program publicly, while privately maneuvering to secure their market share in a post-Cooperative Program world. If those leaders turn to generic, even egalitarian, evangelicalism for funding, then the real loss will be our conservative and distinctly Baptist missions and ministry in the world.

It doesn’t have to be this way. We can course correct. But it will take leadership, messenger will, and patience.

And maybe even a little bit of that Orlando magic.

~~~~~

Appendix A: Cooperative Program Giving Since 2000

9. All of these numbers are drawn from “Total Cooperative Program Giving” in their respective Southern Baptist Convention Annual, which is an annual overview of the previous year. See Southern Baptist Convention, Annual of the Southern Baptist Convention, 2000–2025 (Nashville: Executive Committee, Southern Baptist Convention), accessed March 1, 2026.

10. Federal Reserve Bank of Minneapolis, Consumer Price Index, 1913–, accessed March 1, 2026. The inflation adjustments are calculated using annual average Consumer Price Index for All Urban Consumers (CPI-U) values. For each fiscal year (assumed October 1 to September 30), the effective CPI is a weighted average: 25% of the calendar year CPI for the fiscal year’s starting calendar year and 75% for the ending calendar year. The base for FY2024–25 is similarly weighted.

| Fiscal Year | Nominal CP Giving9 | Inflation-Adjusted (FY2024–25 Dollars)10 |

|---|---|---|

| 2000–01 | $487,257,630 | $886,137,046 |

| 2001–02 | $501,772,139 | $895,601,667 |

| 2002–03 | $501,199,697 | $876,123,640 |

| 2003–04 | $499,865,760 | $851,909,223 |

| 2004–05 | $522,256,617 | $862,383,990 |

| 2005–06 | $533,464,682 | $853,036,763 |

| 2006–07 | $539,608,678 | $838,342,857 |

| 2007–08 | $548,205,099 | $822,050,637 |

| 2008–09 | $525,866,995 | $783,412,009 |

| 2009–10 | $500,410,514 | $736,907,472 |

| 2010–11 | $487,884,065 | $699,147,483 |

| 2011–12 | $481,409,006 | $674,088,522 |

| 2012–13 | $482,279,059 | $664,471,062 |

| 2013–14 | $478,700,850 | $649,400,771 |

| 2014–15 | $474,272,984 | $640,271,031 |

| 2015–16 | $475,212,293 | $635,304,710 |

| 2016–17 | $462,662,332 | $606,921,140 |

| 2017–18 | $463,076,368 | $593,409,360 |

| 2018–19 | $462,299,010 | $580,893,099 |

| 2019–20 | $455,553,027 | $564,707,434 |

| 2020–21 | $457,928,996 | $546,626,570 |

| 2021–22 | $457,417,314 | $509,285,277 |

| 2022–23 | $449,039,992 | $476,053,833 |

| 2023–24 | $446,641,957 | $458,688,168 |